Most people assume their family can automatically manage their finances if something happens to them. In reality, that’s not how the legal system works.

Without a financial power of attorney, even your closest family members may not have the authority to handle your financial matters. This can lead to delays, legal complications, and unnecessary stress during already difficult times.

Let’s break down what really happens—and how you can avoid these risks with proper planning.

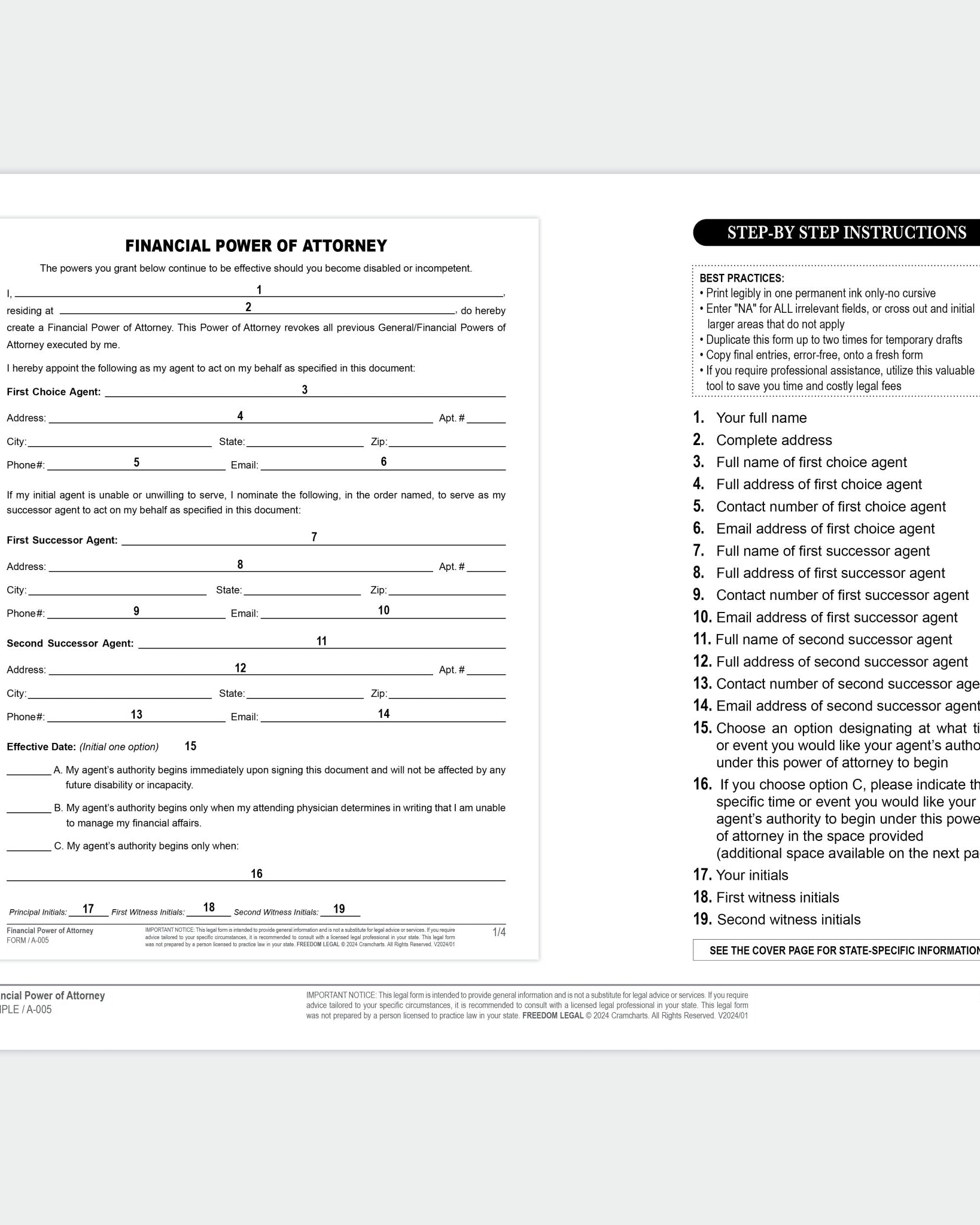

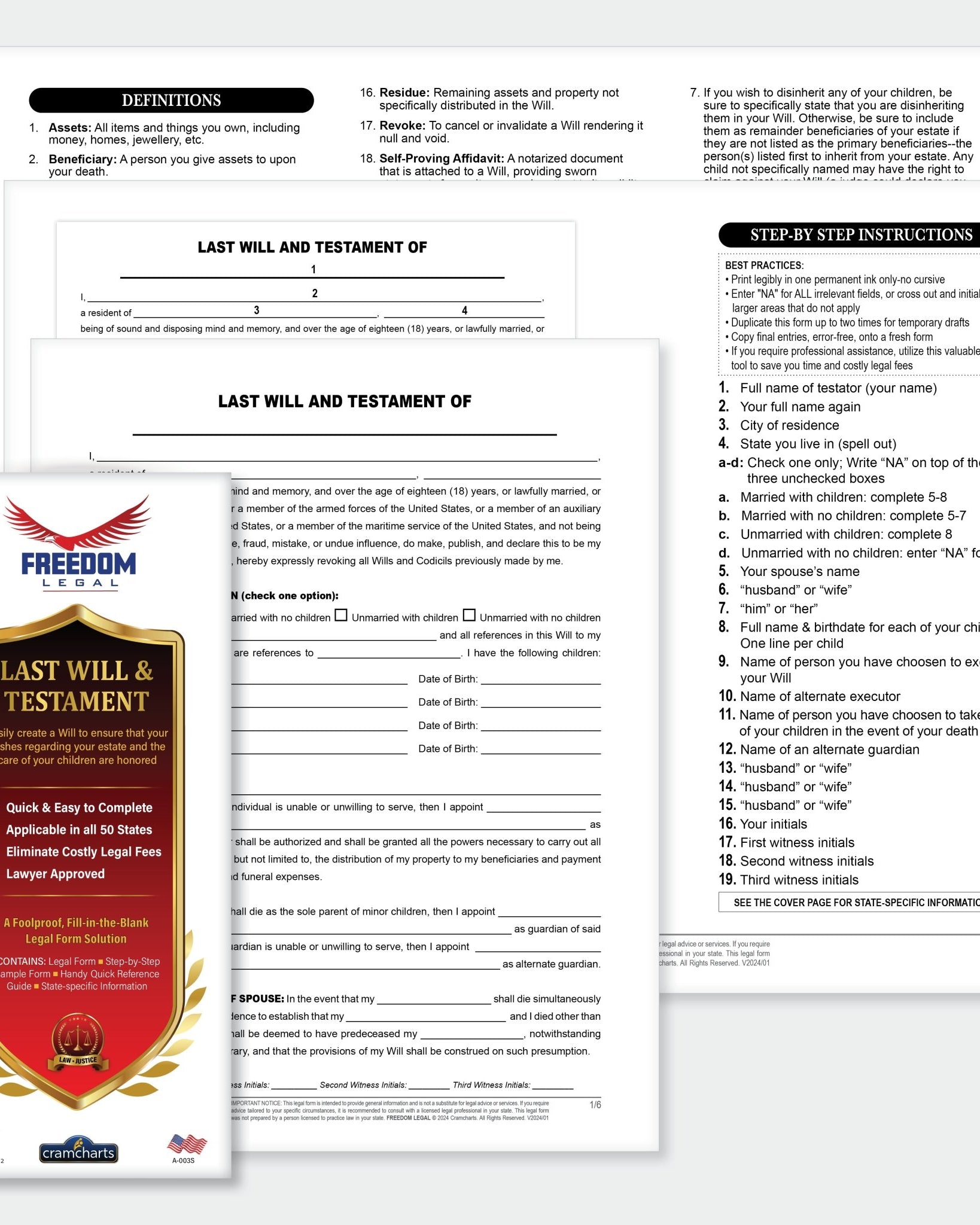

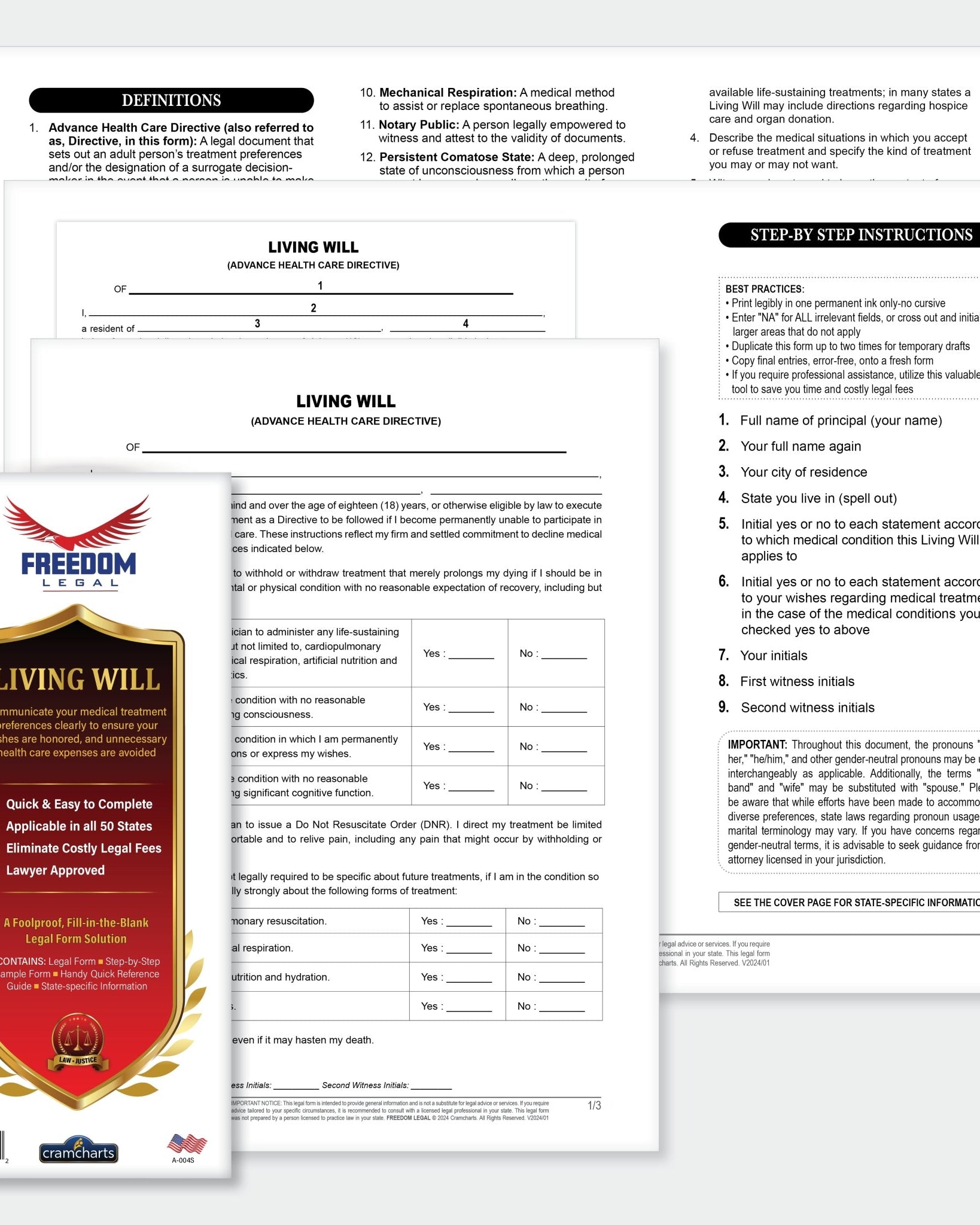

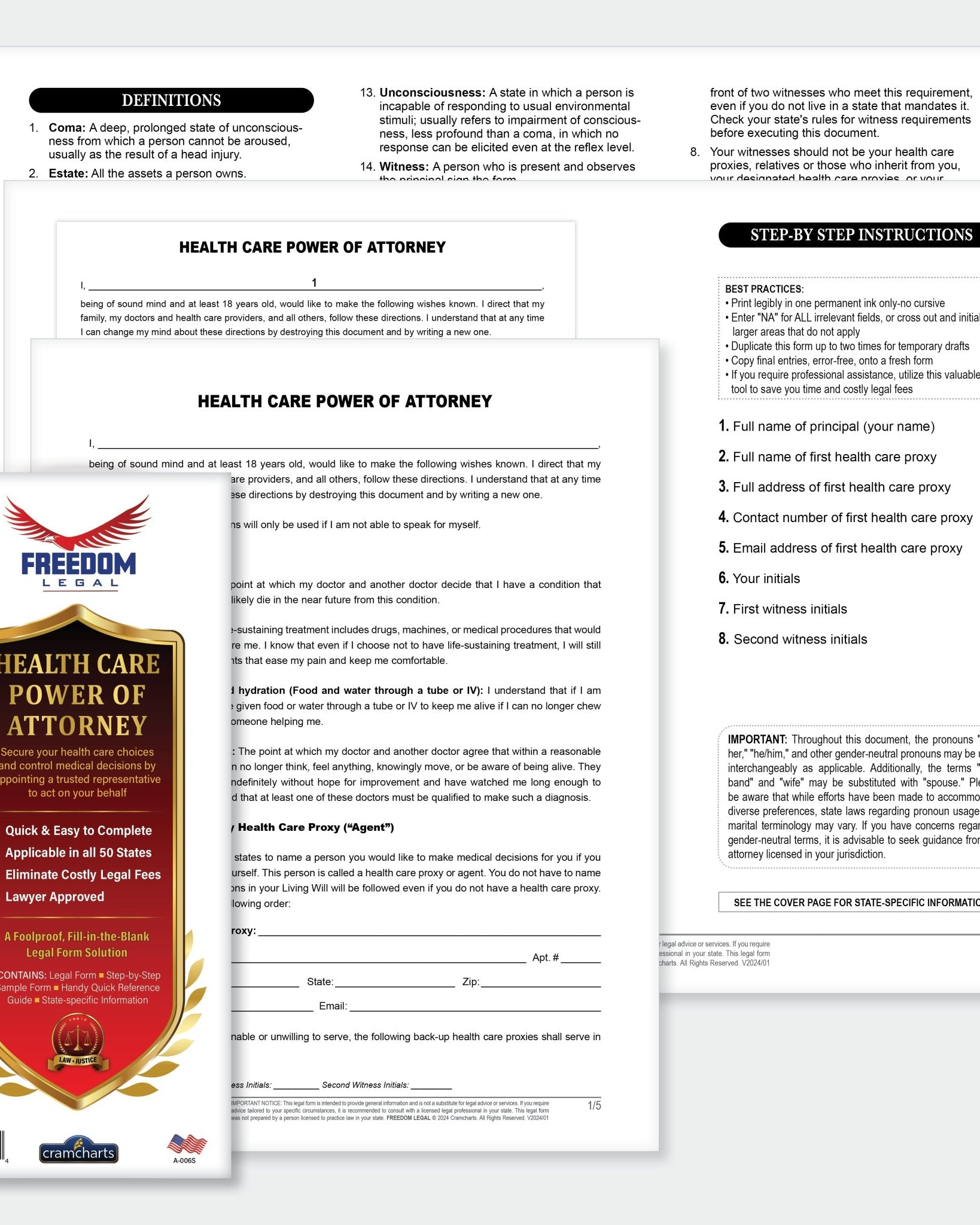

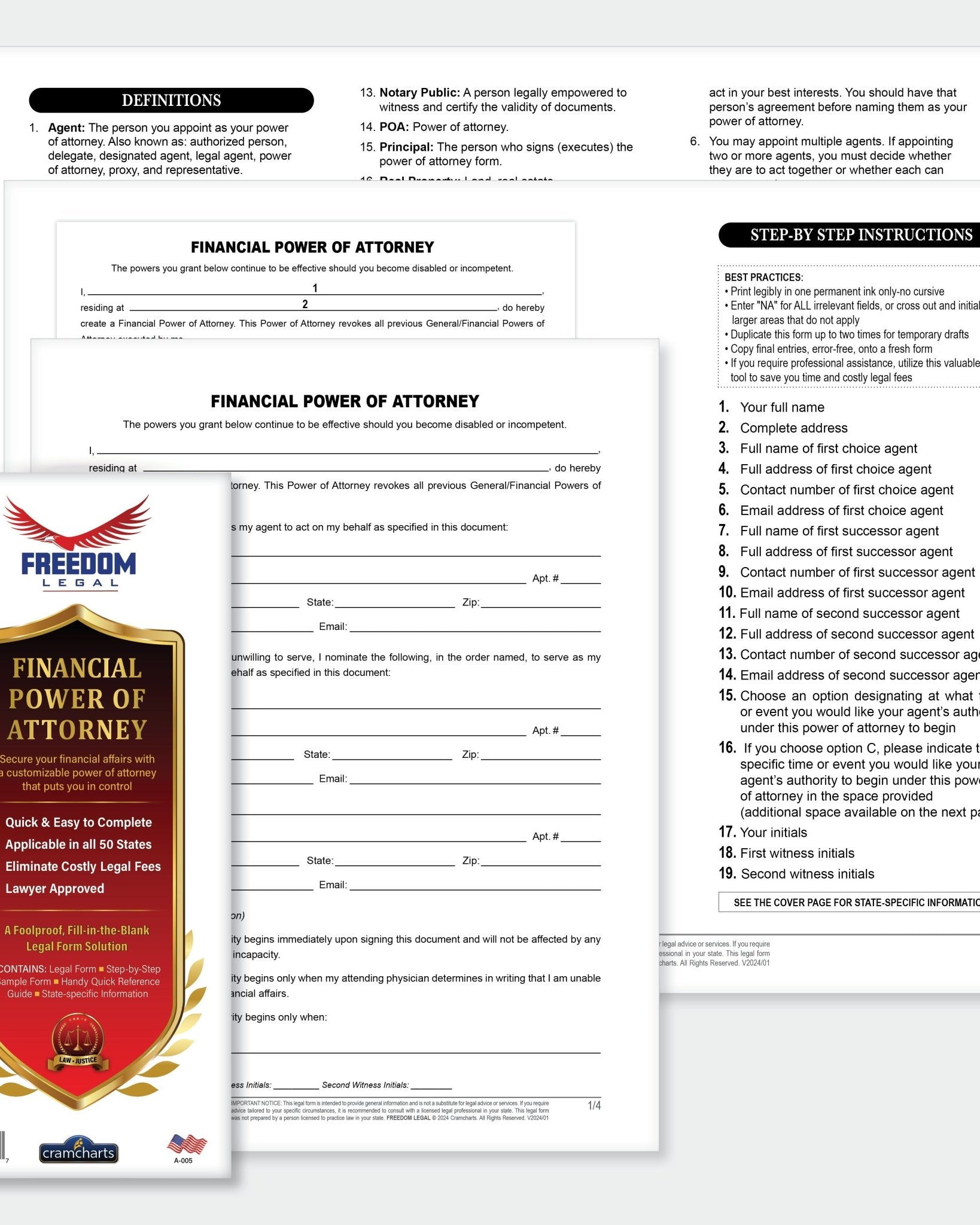

What Is a Financial Power of Attorney?

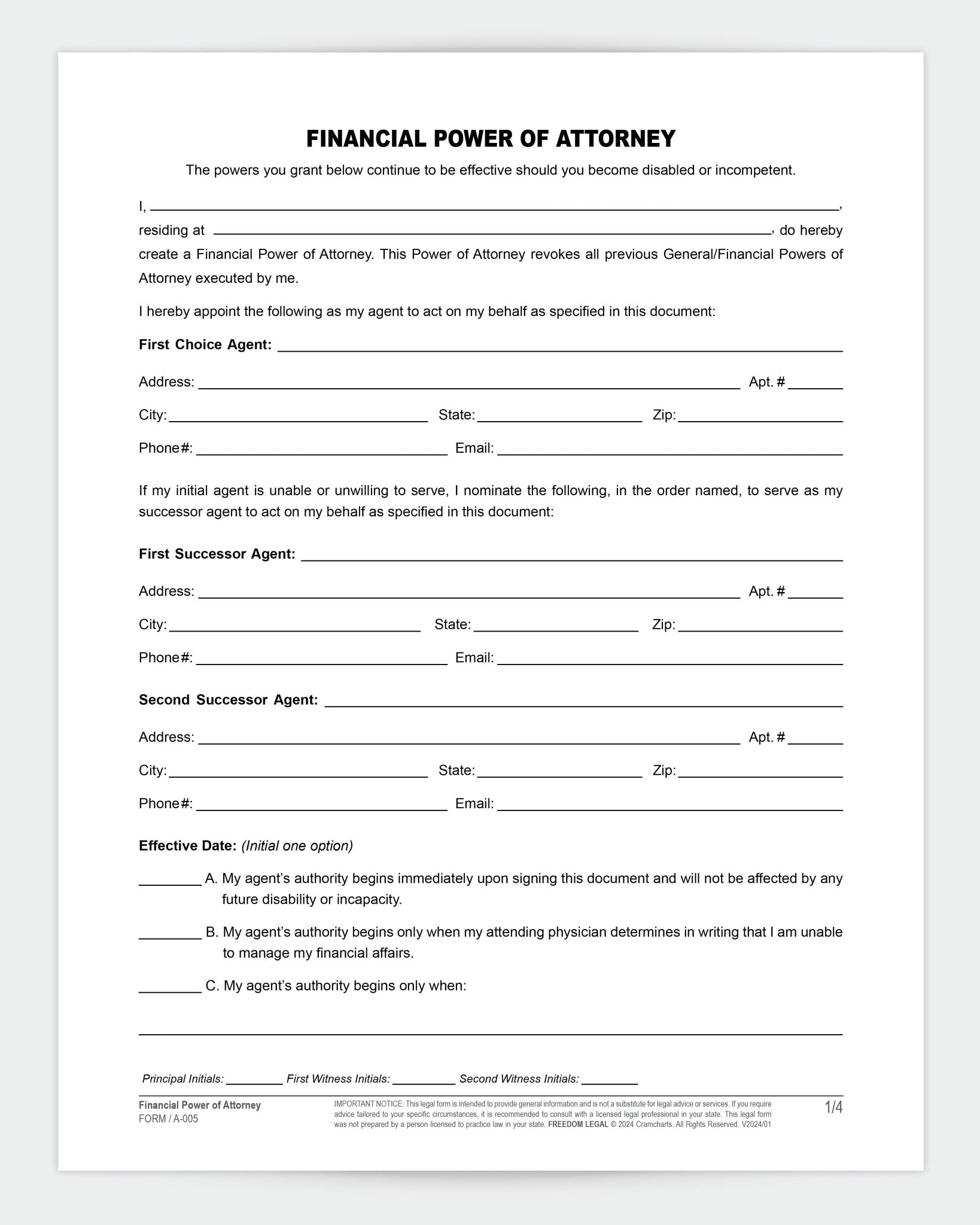

A financial power of attorney is a legal document that gives someone you trust the authority to manage your finances if you’re unable to do so.

This includes responsibilities like:

-

Paying bills and managing expenses

-

Accessing bank accounts

-

Handling investments

-

Managing property or business transactions

-

Filing taxes

The word “durable” means the document remains valid even if you become incapacitated.

Why Not Having One Can Be Risky

Ignoring this document might seem harmless—until a real-life situation proves otherwise.

1. Your Finances Can Get Stuck

If you suddenly become unable to manage your finances:

-

Banks won’t allow access to your accounts

-

Bills may go unpaid

-

EMIs and financial obligations can be delayed

Even a spouse or parent cannot legally act without proper authorization.

2. Your Family May Need Court Approval

Without a financial power of attorney, your loved ones may have to go through a legal process to gain control over your finances.

This often involves:

-

Filing for guardianship or conservatorship

-

Attending court hearings

-

Paying legal fees

-

Waiting weeks or even months

According to the American Bar Association, this process can be time-consuming and emotionally exhausting.

3. You Lose Control Over Who Handles Your Money

When the court appoints someone, it may not be the person you would have chosen.

This can create:

-

Family conflicts

-

Misaligned financial decisions

-

Lack of trust or transparency

With a financial power of attorney, you decide in advance who manages your finances.

4. Business and Investments May Suffer

If you’re a business owner or investor, delays in financial decisions can result in:

-

Missed opportunities

-

Operational disruptions

-

Financial losses

Professionals who actively manage money are especially vulnerable without this document.

5. Emotional and Financial Stress for Your Family

During emergencies, your family should focus on your well-being—not legal paperwork.

Without proper planning, they may face:

-

Confusion about next steps

-

Financial uncertainty

-

Additional stress during critical moments

Real-Life Scenario: Why This Matters

Consider a working professional who suddenly faces a medical emergency.

Without a financial power of attorney:

-

Their spouse cannot access funds

-

Investments remain unmanaged

-

Bills pile up

With it, everything continues smoothly—ensuring stability when it’s needed most.

Who Should Have a Financial Power of Attorney?

This isn’t just for retirees. It’s essential for:

-

Working professionals

-

Business owners

-

Married couples

-

Parents managing household finances

-

Individuals with investments or assets

If you handle money, you need a plan.

How Cramcharts Makes Legal Planning Simple

Legal documents can feel overwhelming, especially if you’re not familiar with legal terminology.

That’s where Cramcharts helps.

The Financial Power of Attorney resource is designed as a quick-reference guide that simplifies complex legal concepts into easy-to-understand formats.

Key Benefits:

-

Breaks down legal information into clear, structured points

-

Helps you understand what to include in your document

-

Saves hours of research

-

Reduces confusion and mistakes

-

Improves decision-making confidence

Whether you’re a professional, student, or family decision-maker, this tool makes legal planning faster and more practical.

Strengthen Your Legal Planning with the Right Tools

A financial power of attorney works best when combined with other essential legal documents.

For example, a family law legal planning kit helps you organize broader legal responsibilities and ensures your family is fully protected.

Similarly, having a last will and testament ensures your assets are distributed according to your wishes.

Together, these tools create a complete legal safety net—covering both your lifetime and beyond.

How This Saves Time, Money, and Stress

Planning ahead with a financial power of attorney:

-

Eliminates delays during emergencies

-

Prevents legal expenses

-

Ensures immediate access to funds

-

Protects your financial stability

-

Reduces stress for your loved ones

It’s a simple step with long-term benefits.

Best Practices for Creating a Financial Power of Attorney

To make your document effective:

-

Choose someone trustworthy and responsible

-

Clearly define their authority

-

Keep the document accessible

-

Inform your family about it

-

Review and update it when needed

Organizations like the Consumer Financial Protection Bureau recommend proactive financial planning to avoid unnecessary complications.

FAQ (People Also Ask)

1. What happens if I don’t have a financial power of attorney?

Your family may need court approval to manage your finances, causing delays and legal costs.

2. Is a financial power of attorney only for older adults?

No. Anyone with financial responsibilities should have one, regardless of age.

3. Can I choose who manages my finances?

Yes, and that’s the main advantage—you stay in control of who makes decisions on your behalf.

4. Does this replace a will?

No. A will works after death, while a financial power of attorney works during your lifetime.

5. How often should I update it?

Review it every few years or after major life events like marriage or financial changes.

Key Takeaways

-

Without a financial power of attorney, your finances may become inaccessible

-

Court involvement can delay important decisions and increase costs

-

This document ensures your finances are managed by someone you trust

-

Combining it with other legal tools strengthens your overall planning